LONG TERM STANCE (6-12 MONTHS): Bull Market

SHORT TERM STANCE: correction

INFLATION FORECAST OVER NEXT 6 MONTHS: moderate inflation

INVESTMENT STANCE: 50% cash, 50% stocks

STOCK CRASH POTENTIAL (NEXT 1-6 MONTHS): LOW

ECONOMY: medium growth

Next Monthly Report: May 11

April 16, 2024

Disclaimer: Do not trade off of this advice. This blog is for informational purposes only. Any investment advice are just suggestions. The author has no experience working in the financial industry.

Stocks

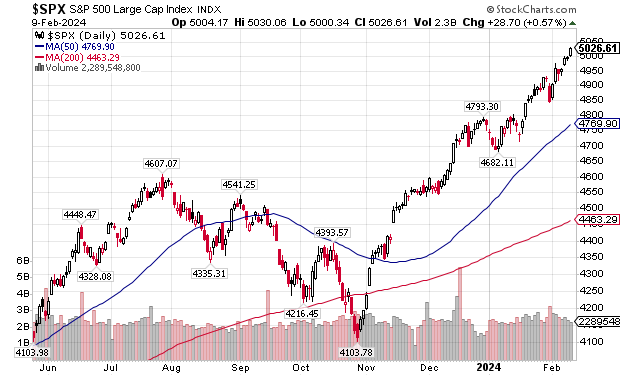

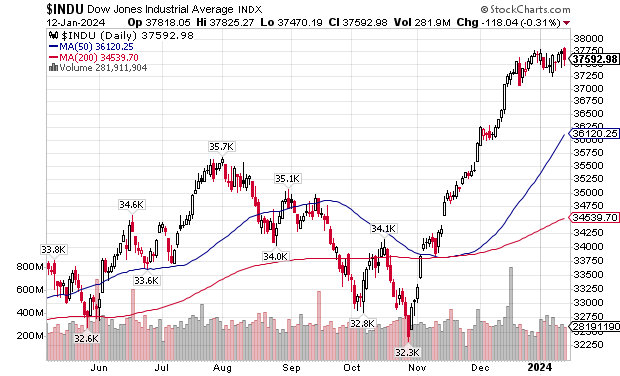

Markets are entering a correction. This was forecasted in the previous report. Stocks are still in a bull market, however. The Dow Industrials had been nearing the psychologically important 40k level and turned down. It is currently 5.5 percent below it’s all time high. The market will probably hit the 200 day moving average before bouncing.

As for the S&P 500, it is nearing the psychologically important 5000 level. My bet is that it will hit the 200 day moving average as well. Also, the 4650 level is roughly a 50 percent retracement of the late October low, which coincides with the 200 day MA.

In the March report:

(There) has been some fracturing in the markets. Less and less stocks have joined the broader market in making new highs. This indicates a pullback is coming soon.

The market had been making new highs, but less and less stocks were making new highs.

One month later . . .

I had also noted:

(There) remains a non-confirmation between the Tranports and the Industrials, which is a Dow Theory violation. The Industrials made new highs while the Transports didn’t. The Transports have performed poorly since December.

Interest rates

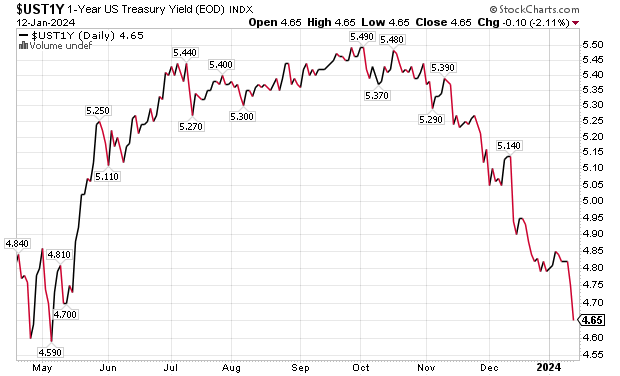

After declining from October to December, Treasury yields have gone up. I had predicted in March that rates would go back down soon. It had looked like a corrective channel.

That did not happen. In fact yields on Treasury notes have gone parabolic!

However, I believe that rates will go back down again after the parabolic rise ends. Some notes could make new highs in yields. It could be the last hurrah for high interest rates for awhile.

I would be investing in Treasury Notes now, so you can lock in the high rates. I do believe that interest rates over the long-term (5-15 years) are going to continue upward. This may not bode well for stocks over the long term.

See also:

The End of the 40-Year Bull Market in Bonds. What’s Next

R.I.P Bond Bull Market , 1981-2021

M2 Money Supply is Shrinking

Seldomly will you hear in the media that the money supply is actually shrinking, which is the first time sustained shrinkage (1993 and 1995 had brief spurts into negative territory) has happened since 1932, which was the era of the Great Depression. Even the 2008 financial crisis did not produce a negative growth rate in the money supply. The M2 annual growth rate is -0.92 percent as of this past March. This is a steady improvement and it may well be in positive territory by the summer. M2 growth bottomed at -4.8 percent this past April.

https://www.longtermtrends.net/m2-money-supply-vs-inflation/

Conclusion

Markets are correcting right now but over the next couple of years, stocks will probably go up, as long as interest rates do not rise appreciably. My prediction is that this decade will be a sideways pattern for stocks, marked with rallies and declines. American income and employment rates will hold up but the cost of living expenses will continue to eat into wealth. It will be an era of “invisible” decline, much like what we saw during the past 50 years. Despite this being a bull market, there are few bargains out there.

Next monthly report: May 11